Table of Contents

India’s rapid rise to enterprise software prominence has been fuelled by a virtuous cycle of innovation across traditional sectors like manufacturing and finance, and new economy domains such as consumer internet and digital health.

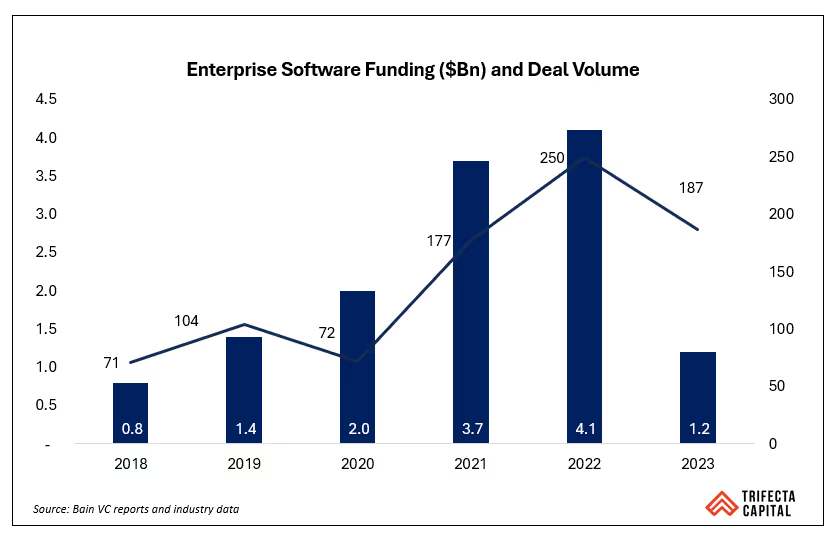

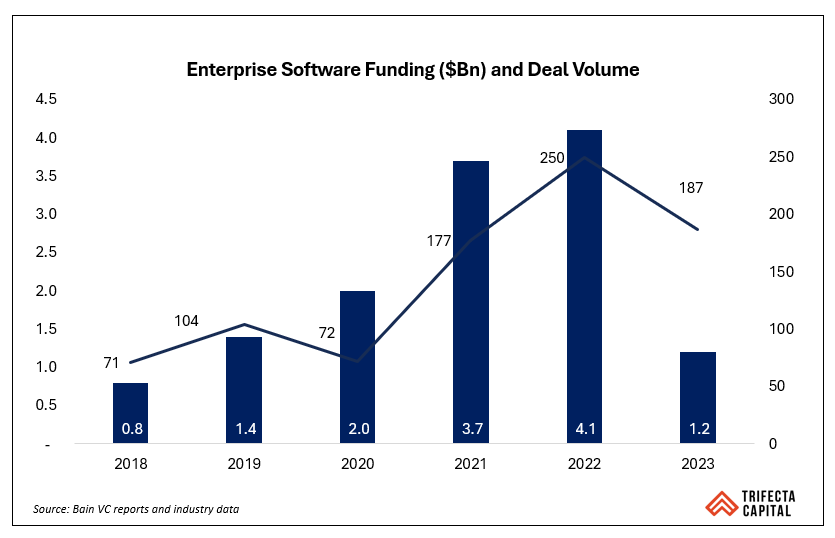

Productivity gains from this cross-pollination have solidified India’s position as an IT services powerhouse and a global leader in Enterprise Software. With over 2,000 companies, including 25 unicorns, India is now the world’s second-largest SaaS ecosystem, capturing 6-8% of global annual revenue. Investments peaked in 2021 and 2022 with over $3.7Bn and $4.1Bn of capital deployed across early and late stages, dropping to $1.2Bn in 2023 and stabilizing to over $1.5Bn in 2024.

Even as a consumer of SaaS products, India has come a long way from being a country that has invited skepticism regarding domestic software spending. Salesforce has crossed $1Bn in revenue and even experienced 35% growth YoY for new business (as of March '24) in the country. India has been a key go-to-market for Slack both for free user base and a paid customer base.

Despite experiencing medium-term pain over the last few years we are optimistic about the prospects this sector holds from a capital markets standpoint.

- Look East for public market exits: With the exception of Freshworks, no other Indian SaaS company has been listed in the US public market. The bar to list in US public markets at a multiple north of 9-10x (LTM EV/Revenue) is also becoming increasingly steep. However, the positive reception of Rategain, TBO Tek, and Unicommerce on the Indian bourses holds promise for the rest of the cohort of mature SaaS companies.

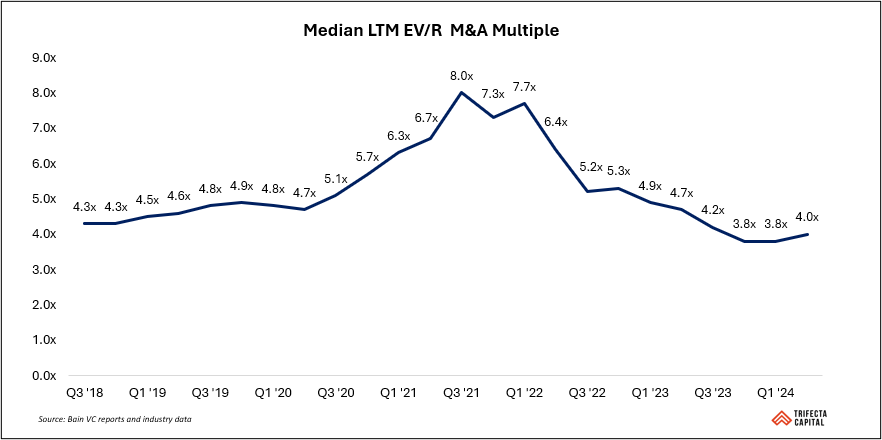

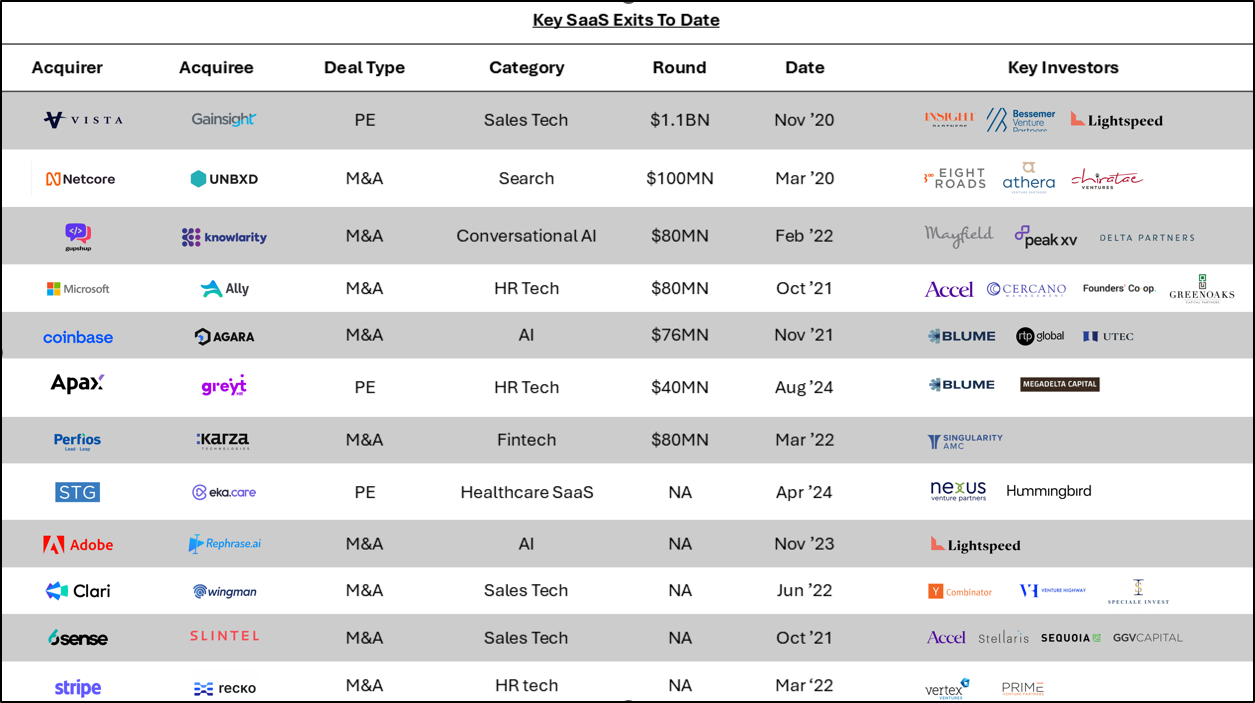

- Valuation convergence invigorates M&A activity: Even on the private markets side the recent acquisitions of greytHR and Eka Care have created renewed optimism towards strategic and PE exits. The convergence of the Median SaaS M&A multiples (went from 8x in mid-2021 to 4x in mid-2024) and public markets multiples (went from 14.4x in mid-2021 to 6x in mid-2024) is indicative of growing M&A momentum.

Public Market Performance

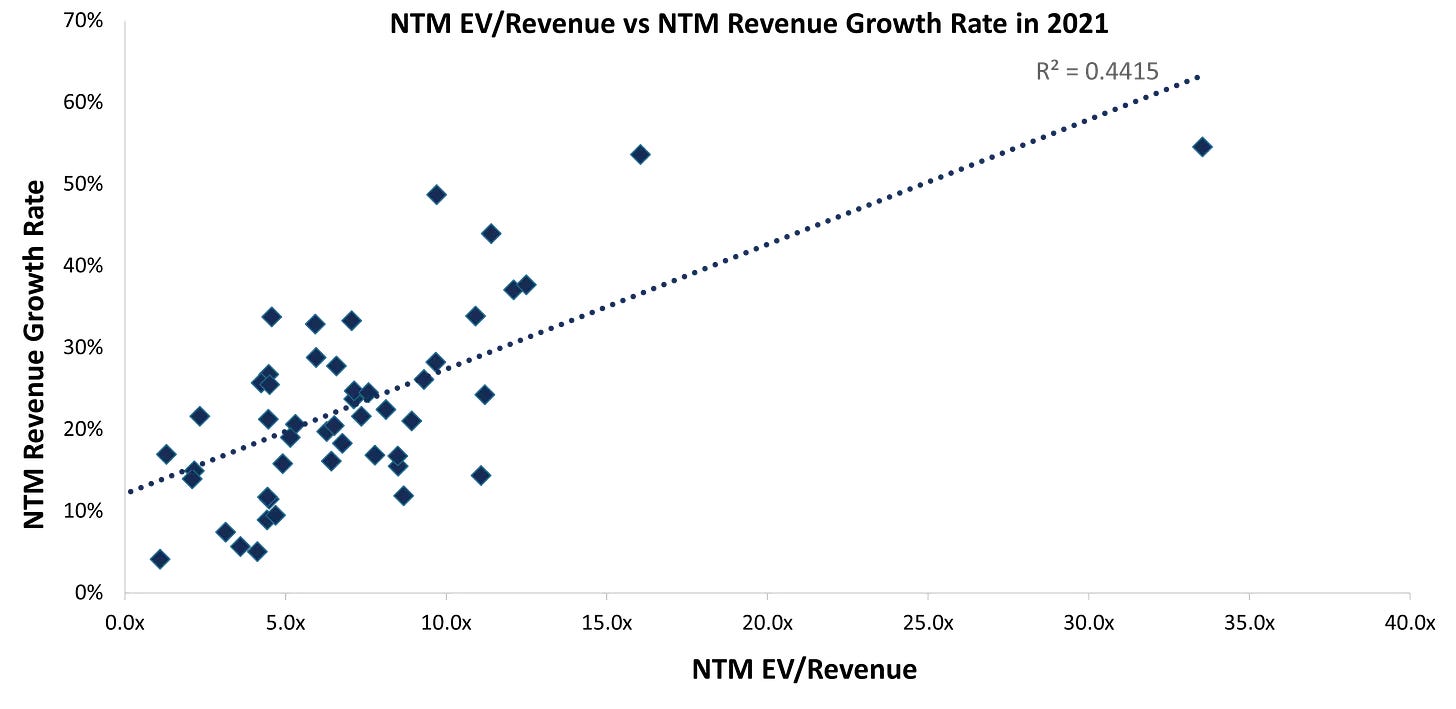

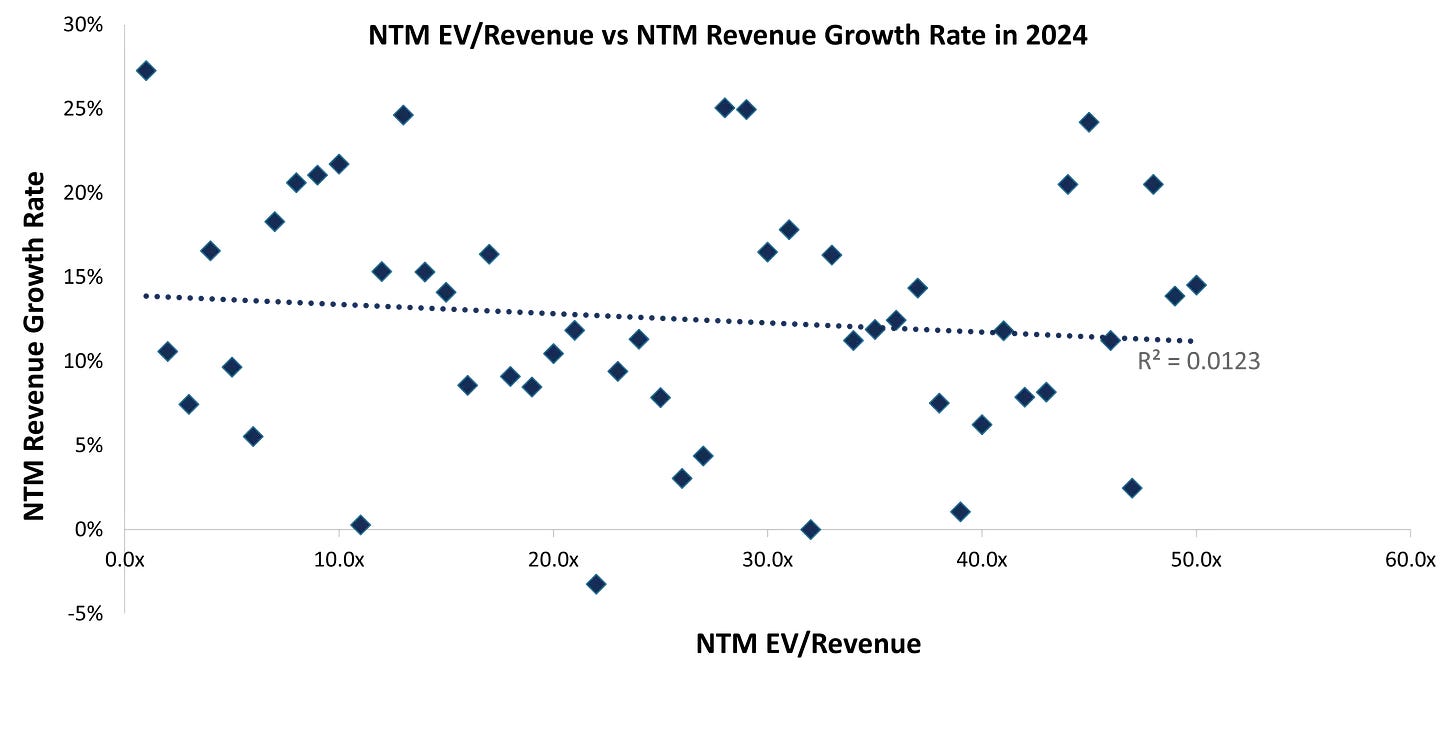

An analysis of a basket of over 45 US Public SaaS companies shows that the correlation between revenue and valuation is not as straightforward now (2024) as it used to be in the 2021 era. While profitability is certainly the other key driver, the margin expansion journeys have not been sufficiently dramatic to compensate for the trade-off on revenue growth. The absolute revenue base of companies have also become a key point to consider.

Private Market Performance

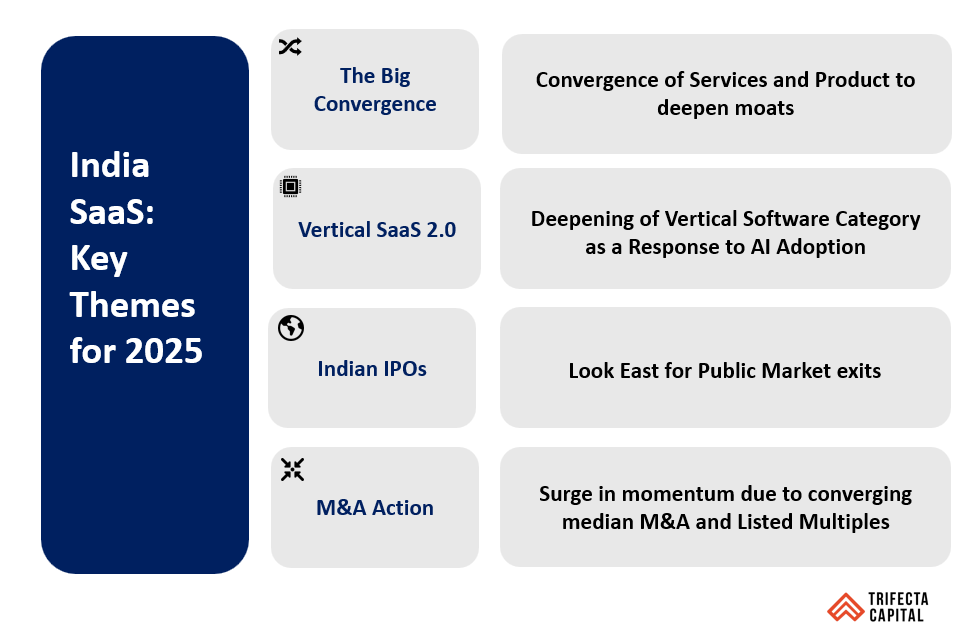

Three key themes stand out to us as dominant categories in this ecosystem that is undergoing one of the biggest technological transformational shifts (AI).

- Vertical Software 2.0: Vertical software in India have come of age with businesses that sell to India plus the rest of the World (Classplus, Infinite Uptime) as well as those that are focused on International markets from Day 1 (Zenoti, Toddle) These businesses also demonstrate greater stickiness by embedding in core workflows and are also characterized by lower competition. Vertical Software is uniquely poised to leverage AI with its access to proprietary data and domain-specific use cases. We also believe this is catalyzing adoption in some industries like construction and manufacturing that had been slower to adopt vanilla Vertical SaaS tools.

- BFSI rails: The past decade has witnessed a seismic shift in India's BFSI landscape, driven by UPI, technological advancements and evolving customer expectations. Software tools have come in handy right from the data aggregation solutions (Perfios, Idfy) to debt collection tools (Credgenics) to agentic workflows for customer support (Yellow AI). Driven by record AI spending in the past year, demand within this segment continues to grow.

- Convergence of Services and Product: As a country that powers almost 55-60% of all digital workflows, India has an intuitive understanding of servicing legacy players who are willing to allocate considerable budgets for digital transformation, cloud and AI capabilities. We believe that several mid-sized IT services companies have initiated well-timed product/platform pivots leveraging their existing customer base and sales efforts to create more revenue potential and margin improvement.

Funding Outlook

Enterprise software funding in India has gone from $0.8Bn in 2018 to $1.2Bn in 2023 to over $1.4Bn in 2024. With over ten $100M ARR companies, the ecosystem has backed several investments in both horizontal and vertical software. The last 3 years have also witnessed the rise of several emerging managers, who have set up specialized funds (Boldcap, Neon Fund, Foster Ventures, Ahead VC) to strengthen the Indo-US corridor. This is also reflected in the uptick in deal volume brought on by the rise in the number of Pre-Seed, Seed, and Series A deals.

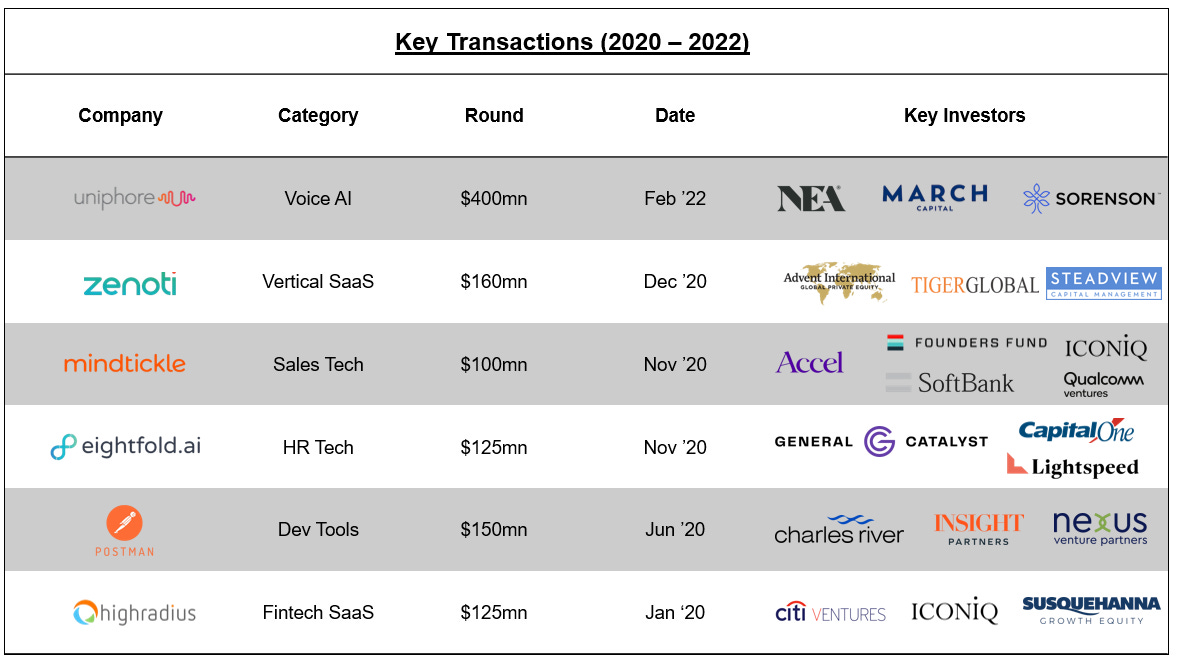

The 2020-22 period was marked by several $100M+ rounds spurred by the entry of PE/Global growth equity funds. Companies like Uniphore, Postman, and Eightfold were all raised from international investors like NEA, Capital One, and Charles River marking a new age in the SaaS investing landscape. 2022-24 was relatively silent from a late-stage investing standpoint, given the global macro, spending cuts, and time taken to grow into the revenues that justify valuations they received during the 2020-22 era.

The rise of AI has led to an acceleration of digital transformation efforts by companies worldwide. We are also witnessing mid-sized Indian IT Services companies rise to the challenge by building platform and product capabilities that help create operating leverage beyond what is expected with traditional IT Services businesses. Funds like TPG, A91, and Norwest Venture Partners have already made bets on such businesses by investing in companies like, Xpedeon, Cerebral Technologies, and Altimetrik, that were bootstrapped until this point compared to other VC-backed companies of the same maturity. Growth equity in such bootstrapped companies can provide vital booster fuel for accelerated growth and create potential upside for investors through multiple and margin expansion.

From an exit point of view, most mature SaaS companies have chosen to remain private until now. Businesses like Amagi have provided exits through secondaries for its earlier investors - Emerald Media, which led a $35M Series D round made a 3x return for its investors through a secondary exit in Sep-2021. However, many other investors in scaled SaaS assets are now looking for the best path to liquidity for their investments given the fund vintages they backed these companies from.

Acquisitions by strategic (PE-backed and otherwise) and private equity players have created some liquidity for investors. PE funds like Vista, STG, and Apax as well as PE-backed Strategics like Clari, and Perfios have all made notable acquisitions in the ecosystem. Strategic M&A by international companies like Adobe, Microsoft, and Stripe also attest to the quality of product innovation at these companies.

The median revenue multiple for SaaS M&A across the world stands at 4x, at a 33% discount to the median for public SaaS companies (6x as of June 2024).

We believe that 4 broad themes will dominate the landscape over the next 18 months

- Convergence of Services and Product/Platform companies as a response to the AI paradigm shift

- Deepening of the vertical software category accelerated by the adoption of AI in more traditional industries like Construction, and Manufacturing.

- Riding on the success of Unicommerce, and TBO Tek listings, the next wave of companies will list on Indian bourses serving Indian and International customers.

- Consolidation in specific categories like Fintech or HR Tech. With a considerable pool of companies in the $3M-$15M category, the interest from PE funds and PE-backed strategics, and increasing buying complexity in B2B purchases, we could be entering an era of M&A in select industries.

As investors in the new economy, we are bullish on the enterprise software landscape in India. It's a market brimming with untapped potential. From AI-driven platforms to cloud-native applications, the diversity and scale of these startups is truly impressive.

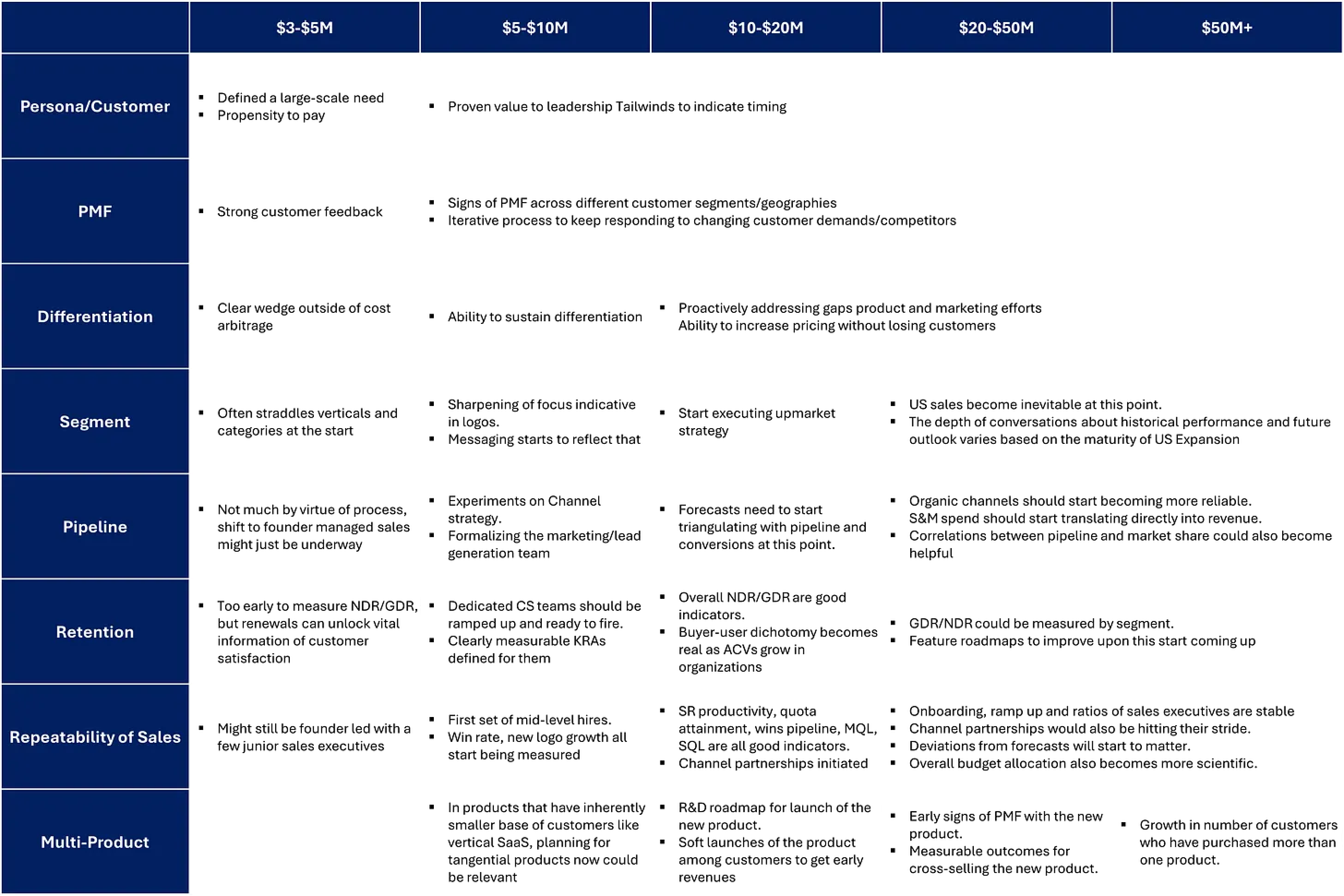

We have therefore decided to put together our framework for evaluating SaaS Companies starting from early-growth to late-stage maturity.

Here’s a glimpse of what we are referring to, head to the next article for more!